Quantitative Easing: a massive giveaway to the Rich

But don’t blame Wall Street or capitalism

In Unmasking Inflation, I described how Quantitative Easing (QE) has simultaneously inflated asset prices to record highs while slashing interest rates to their lowest levels in history. As a result, the monthly cost of accumulating savings has more than tripled, putting financial independence out of reach for most people. Traditional savers and conservative investors (aka the middle class) are the biggest losers.

In contrast, the Fed’s policies have also created big winners. Just as QE has unfairly penalized savers, it has unjustly rewarded the owners of stocks, bonds, and real estate. This favored class includes professional investors, financiers, asset managers - all those who use money to make money. Collectively, we often refer to these folks as “Wall Street.”

To understand how QE benefits the wealthy, recall how new money reaches the owners of financial assets. Money is created by commercial banks when they buy bonds (usually government or mortgage-backed) from investors. Under QE, the Fed then buys these bonds from the banks, bidding up bond prices and driving down interest rates.

Yield-hungry investors, who now have cash instead of an interest-bearing bond, are motivated to speculate in other assets like corporate bonds, stocks, and real estate. As long as the banks and the Fed continue repeating this process, more cheap money is available for investment. Wall Street can borrow heavily against inflated assets at interest rates so low some call it “free money.”

Commercial banks love this racket because the Fed ensures that they profit from their bond trades. Investors love it, too. As long as the banks and the Fed keep buying their bonds, they can reinvest their gains in speculative assets, driving prices higher.

As an old Wall Street mentor of mine said, “Money chases the inflating asset.”

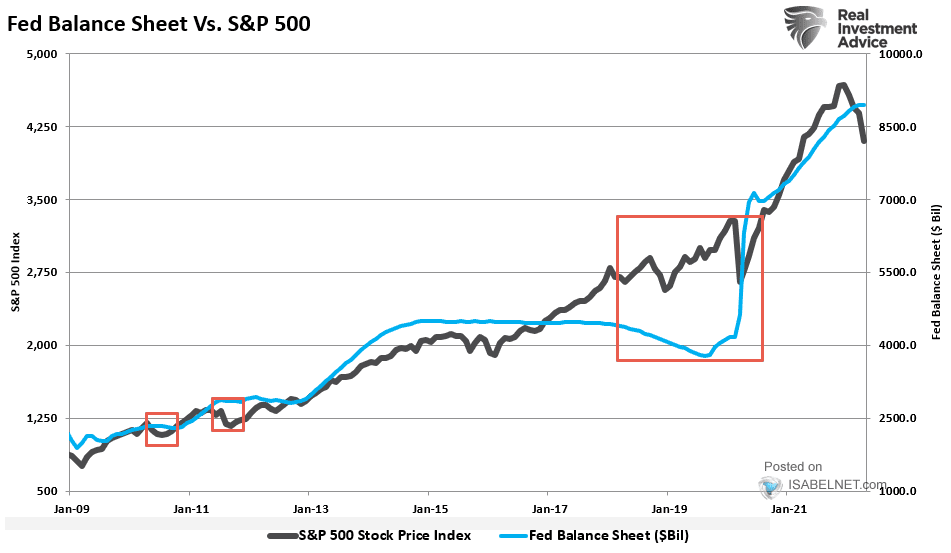

The graph below captures the story of Quantitative Easing. In successive waves of bond buying, the Fed has increased its bond portfolio from $800 Billion in 2010 to $8.45 Trillion as of this writing. As the Fed’s assets grow, the price of the S&P 500, a broad-based index of stock prices, rises as well.

Source: Real Investment Advice

{kind=link}

QE has been a windfall for the banks and Wall Street, but not for Main Street. How did the Fed produce such a lopsided outcome?

Quantitative Easing was the brainchild of former Fed Chair Ben Bernanke, who mapped out his economic recovery plan in a Washington Post article on November 10, 2010:

“Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.”

Bernanke proposed QE as a temporary stimulus for a depressed economy. Increased confidence and spending would create an economic tide lifting all boats, even the little ones.

Perhaps Bernanke did not foresee that the Main Street boats would founder while the yachts of Wall Street sailed into the sunset. His bold claim that a “virtuous circle” would somehow “boost consumer wealth” was at best an untried theory.

Whatever he believed about Main Street’s prospects, Bernanke was well aware that QE’s initial effect would be a big payout to Wall Street. Unquestionably, this aspect of his policy was intentional.

In the early days of QE, Wall Street was close-lipped about its financial windfall. But in 2015, hedge fund manager David Tepper, founder of Appaloosa Management, broke the ice. By then, all the world’s other major central banks – including the European Central Bank, the People’s Bank of China, and the Bank of Japan – were busy mimicking the Fed, aggressively purchasing bonds and even stocks with newly-created money.

“This will create a tailwind for equities,” Tepper told Bloomberg News. “It’s kind of hard to fight money…Don’t fight the Fed. Now you’ve got four Feds. Don’t fight four Feds.”

After just three years of QE, Tepper’s annual income reached $3.5 Billion. Tepper, a brilliant investor, scored better than many, but thousands of other traders, large and small, also made fortunes, large and small.

Today, a decade after Bernanke’s op-ed, massive bond-buying is still the Fed’s one-trick pony. Higher stock prices continue to benefit the wealthy, but the promise of “boosted consumer wealth” never materialized. Instead, the average Joe faces persistently high unemployment and rising consumer prices. (Have you noticed the price of gas or bacon lately?)

Despite this asymmetric outcome, the Fed remains dogmatic. Fed Chair Jerome Powell insists his central bank’s policies “absolutely” do not add to wealth inequality. But this is untrue, and Powell knows it.

Bernanke understood the game from the very beginning. So did his successors, Janet Yellen and now Powell, and so did Wall Street. Financial asset managers and traders did exactly what Bernanke wanted, borrowing at low rates, trading securities hand over fist, and driving up prices. What could go wrong?

It took only a few years of QE for the stock market to surpass its highly inflated 2007 pre-crash level. (This happened in March 2013). In the ensuing eight years, the stock market rose another 280%, and the party continues to this day. Fed Chair Powell remains committed to buying $120 Billion in bonds per month (a rate of nearly $1.5 Trillion per year) for the foreseeable future – all with new money conjured out of thin air.

And now, at long last, the consumer is waking up. Many now understand that speculation in the financial markets is their only chance to gain financial independence. Average folks, especially the young, trade cryptocurrencies, “meme” stocks, and “non-fungible tokens.” This trend is not likely to end well.

Although it’s tempting to resent Wall Street’s good fortune, objectivity demands that we distinguish between those who produce their wealth and those who get it by forced redistribution. Let’s call it the Steve Jobs kind of wealth versus the David Tepper variety.

Almost everyone respects the Steve Jobs kind of wealth. For the price of an iPhone, Apple’s customers receive remarkable value. If “wealth” consists of valuable goods and services, then the wealth Jobs created for his customers dwarfs the massive profits he earned for himself.

But just as most people respect Jobs’ wealth, they despise Tepper’s. These opposing views seem reasonable at first glance because the difference between Jobs’ and Tepper’s fortunes could not be starker. Jobs won his wealth in a competitive marketplace of technological innovation, while Tepper’s windfall came from a government policy intentionally designed to reward those who already owned financial assets.

But the US Federal Reserve, not Wall Street, caused this skewed economic outcome. Wall Street grew fat, but it was force-fed like a barnyard goose. And, like the fattened goose, Wall Street did not ask for the Fed’s sustenance.

Financial markets were not always rigged to benefit the rich. Wall Street grew up when Fed influence was less critical, a time when success depended on price discovery derived from competitive trading. In those better times, Wall Street traders and financiers served a highly productive economic function, directing the accumulated savings of investors to their most important uses. Until QE came along, the market, not the government, chose winners and losers on Wall Street.

So, don’t blame Wall Street for the injustice wrought by QE. Blame the Fed – or better yet, blame Congress, which can change the laws that empower the Fed.

Some will blame QE’s unfair wealth transfer, not on Wall Street, but on capitalism itself. But that’s also wrong because authentic capitalism is nowhere to be found at the Fed.

Capitalism’s essential trait is private (non-government) ownership of the means of production. Under genuine capitalism, all economic relationships, including financial transactions, are voluntary. Force or fraud, initiated by citizens or by the government, is illegitimate and should be illegal.

Under genuine capitalism, government exists to protect life and private property. Citizens grant their government a monopoly on the use of force, and government uses this delegated power only when necessary to protect citizens from force or fraud. The principles of capitalism require that no one, even the government, disrupts voluntary trade between consenting parties.

The Steve Jobs kind of wealth came from capitalism, or what remains of it. By contrast, the Fed’s perverse transfer of wealth to the rich came from capitalism’s opposite: government central planning imposed on financial markets by force.

Quantitative Easing is merely a species of despotic behavior that favors the wealthy while penalizing almost everyone else. When a central bank picks economic winners and losers, it has abandoned capitalism and crossed a new frontier into what I call “monetary fascism.” It’s high time Americans held Congress accountable for the economic injustice wrought by the Fed.

HardmoneyJim No.6