From Cigars to Bitcoin: The Simple Truth About Why Prices Rise

What a neighborhood cigar shop can teach you about the global financial system — and about whether you’re an investor or a speculator.

Why do prices keep going up? Not just the price of one thing, but the price of nearly everything — cigars and cars, houses and groceries, stocks and Bitcoin. It sounds like a simple question. Yet most people, including a great many who spend their entire careers in finance, have never worked through the answer from first principles.

That’s what I want to do here. We’ll start small, in one of my favorite places — my neighborhood cigar store — and build our way up to the global financial system. Along the way, we’ll pass through some of the most spectacular price manias in history: tulip bulbs, Beanie Babies, and Bitcoin. And we’ll keep returning to one question that matters more than almost any other you can ask about money: are you an investor, or a speculator? Because it makes an enormous difference which game you think you’re playing.

[If you find this useful, consider subscribing, or view the video essay version on my Youtube Channel. Either way, you’ll help this work reach more people.]

Part One: Cigar-Store Economics

Start with cigars. Picture a modest shop in your neighborhood — nothing fancy, just good cigars and loyal customers.

Say it sells 1,000 cigars a week at $20 each, for $20,000 in weekly sales. Business is steady. Prices are stable. Supply and demand are in balance.

We can capture that relationship with a simple identity:

D = S × P

Total demand (D) equals supply sold (S) times average price (P). Here, $20,000 = 1,000 cigars × $20.

Rearrange it, and you get price:

P = D ÷ S

Price equals total demand divided by supply — so $20 = $20,000 ÷ 1,000 cigars.

Throughout what follows, I’ll hold supply constant. That lets us isolate the thing we actually care about: the demand factors that push prices up.

Now suppose the owner wants to raise his price to $30, while still selling 1,000 cigars a week. The real question isn’t whether he can post a higher price. It’s whether he can actually sell at that price.

For his customers to pay $30 instead of $20, they have to spend more on cigars — $30,000 a week instead of $20,000. So where does that extra $10,000 come from?

Think about who these buyers are. They’re like most of us: regular incomes, spent on the things they want, with a little saved along the way. At any given moment, their financial lives are roughly in balance — which is just another way of saying their personal supply and demand are in balance. If they’re going to spend more on cigars, the money has to come from somewhere. I count four possibilities.

First, they could dip into savings — money in a bank account or, as the old saying goes, under the mattress. This raises prices, but only for a while. Once the savings are spent, the extra spending stops. Dipping into savings gives you a temporary surge of money and a temporary price spike. It does not give you a permanent increase.

Second, they could cut back elsewhere — eat out less, skip a vacation — to afford pricier cigars. That behavioral shift can produce a lasting increase in cigar spending. But it’s a one-time step up, not an ongoing escalation.

Third, they could get new money from outside — a bonus, an inheritance, a loan. This is genuinely new spending power entering the picture, not just money shuffled from one pocket to another. But once again, a one-time injection buys a one-time increase in demand, and therefore a one-time increase in price.

Fourth, and most important, imagine chronic inflation — new money continually entering the economy and showing up as a steadily rising monthly income. Now the cigar lover can spend a bit more each month, month after month, and the price can keep climbing as more money keeps arriving. This is the only source on the list with no natural stopping point.

But notice something. Every one of those sources speaks only to the buyer’s ability to spend more. Ability alone isn’t enough. You also need willingness.

A cigar lover who lands a windfall won’t necessarily blow it on cigars. He might take a vacation, buy a car, or drop the money into his brokerage account. Whether any of it reaches the cigar store depends on how badly he wants those cigars — how highly he values them against everything else he could do with the money. That’s a question about the buyer’s psychology, not his balance sheet. And it matters just as much as the money does.

So here is the core principle, stated as plainly as I can:

Prices rise when buyers are both able and willing to pay more.

Call these the two pillars of demand. The first is monetary — do they have the money? The second is behavioral — do they want to spend it on this specific thing? Both must stand for a price to rise. You can drown a man in cash, but if he doesn’t want cigars, the shop owner gets nothing. And you can want cigars desperately, but with no money to spend, your desire moves no prices at all.

It sounds obvious. Watch what happens when we carry it into a much larger and more complicated world.

Part Two: Liquidity and the Investment Markets

The logic that governs the price of cigars governs the price of stocks, bonds, real estate, and commodities. The mechanism is identical. Only the scale changes.

So: what drives stock prices higher? The same thing that drove up the cigars. For stock prices to rise, buyers must be both able and willing to pay more than they did before. Where does the extra money come from? The same menu applies. People can draw down savings to buy stocks. They can divert money from other purchases, or sell the vacation home, or invest an inheritance, or borrow to fund a brokerage account.

Or — and this is the crucial addition at scale — new money can be created and directed into the markets. That last mechanism is the subject of my book, A Black Hole in Economics.

Here’s why the distinction matters. The first several sources are all limited. Savings run out. There’s only so much you can divert from other spending. Borrowing has a ceiling. But the creation of new money in a fiat system has no theoretical limit at all. Governments and central banks can, and routinely do, create money in essentially unlimited quantities. And that is the key insight of this whole essay: only continuous money creation can fuel continuously rising asset prices.

You might reasonably object: are investors really cutting back on cars and vacations to pile into stocks? Is that why the market keeps rising? I see no evidence of it. Just the opposite — the prices of food, houses, and cars have all been rising too. Everything is going up at once. That’s not the fingerprint of people sacrificing consumption to invest. It’s the fingerprint of money creation, not reallocation.

The economist Michael Howell, who writes the excellent Substack Capital Wars, has done some of the most rigorous work I know of on how money drives asset prices. He’s built a sophisticated liquidity index that measures the money available worldwide to spend on financial assets, and the correlation between that index and asset prices is striking. The chart above sets his liquidity measure against the MSCI broad index of global stocks. (MSCI = Morgan Stanley Capital International.) More available money seems to translate almost directly into higher asset prices.

It isn’t a perfect relationship. Prices don’t move in lockstep with liquidity — and I’ll explain why in a moment — but the directional link is powerful and well-documented.

The essential point is this. When governments run large deficits, and those deficits are monetized — when the monetary authority essentially prints money to cover the government’s bills — that new money gets spent somewhere. And a large share of it typically flows into financial assets. This is not a conspiracy theory. It’s a documented mechanism with a long historical record. In Chapter 4 of my book, I walk through two clear cases: the excessive money creation behind Japan’s asset bubble of the 1980s, and behind the QE-driven asset bubble of 2009 to 2022.

Part Three: Liquidity and the Willingness to Spend

But money alone can’t explain everything we see in markets. Remember the cigar store. The owner raised his price, and we asked two questions, not one: did customers have the money, and did they want to spend it on cigars?

The same two questions apply to stocks, bonds, Bitcoin, or any other asset. Having the money is necessary. Wanting to spend it on that particular asset is also necessary.

This second element — the appetite, the willingness, the propensity to spend — is much harder to quantify, because it’s psychological. It’s shaped not just by sober personal preference but by narrative, fashion, fear, and greed; by what your neighbor is doing; by what you read on your phone last night. It is the reason markets so often diverge from what a cold reading of money creation would predict.

Here’s a vivid recent example. From roughly 2009 to 2022, the Federal Reserve’s quantitative easing (QE) created enormous quantities of new money and handed it directly to institutional investors — the professional money managers most people just call “Wall Street.” That new money gave them the ability to spend more. And what did they want to do with it? Exactly what every professional investor wants to do when handed more money: invest it. That’s the job. That’s the entire orientation and incentive of the profession. Institutional investors have an almost unlimited propensity to put new money into financial assets.

The result was entirely predictable. Thirteen years of more and more money chasing a limited supply of financial assets pushed up bonds, stocks, and real estate together. People took to calling it the “everything bubble.” There was no magic in it. It was cigar-store economics, writ enormous.

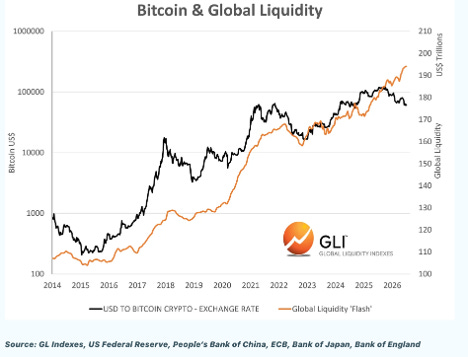

Now look at Bitcoin through the same lens. For most of its history, Bitcoin’s price tracked global liquidity fairly closely. When liquidity rose, Bitcoin tended to surge; when liquidity tightened, Bitcoin fell. Howell’s data documents the relationship clearly. Note how he plots it: the money available to spend on the right axis in trillions of dollars, and Bitcoin’s price on a logarithmic (percentage-change) scale on the left — because the log scale reveals just how sensitive Bitcoin’s price is to changes in liquidity.

Howell believes that liquidity momentum — the rate of change in the money available — is the primary driver of Bitcoin’s price. I read the same chart a little differently. Look at the far right. Something appears to have changed around October 2025. Even as global liquidity kept rising, Bitcoin’s price began to fall, and has since dropped by roughly 50%. According to the chart, there’s still plenty of money sloshing around — so what changed? In my view, what changed was the willingness to spend that money on Bitcoin. Investors’ appetite for Bitcoin, relative to other assets, appears to have peaked and then declined. Why it did is the question the rest of this essay is really about.

Part Four: Speculation Versus Investment

Before we can understand what happened to Bitcoin, we need a distinction I regard as one of the most important in all of finance — and one that is routinely blurred, ignored, or deliberately obscured. What is the difference between a speculation and an investment?

The clearest answer I know comes from Benjamin Graham, Warren Buffett’s mentor and the father of value investing. In 1934, Graham defined an investment as an operation that, on thorough analysis, promises safety of principal and an adequate return. Everything else, he said, is speculation.

Let me put that in plainer language.

An investor buys an asset because the asset itself — the business, the property, the bond — generates real income. Own a stock and you own a slice of a business that earns money; it’s that earning power that justifies the price. The return comes from income: dividends, earnings growth, interest. The investor expects to be paid for owning the thing, regardless of what anyone will offer for it tomorrow.

A speculator buys an asset mainly because he expects someone else to pay more for it later. His return depends on market psychology — on finding the next buyer at a higher price. The asset itself needn’t generate income or serve any use. It only has to be desirable to whoever comes next.

Keynes captured it memorably. He compared speculation to a newspaper beauty contest in which the goal isn’t to pick the most beautiful face, but to pick the face you think everyone else will pick. You’re not judging objective value. You’re guessing at other people’s guesses.

The implications are large. An investor can be wrong about a stock and still recover, because the underlying business keeps producing cash. A speculator who is wrong about timing can lose everything, permanently — because once the crowd stops wanting the asset, there is nothing underneath to catch the fall.

None of this makes speculation evil. Speculators provide liquidity, which markets need. But it is a fundamentally different game from investing, with different rules, risks, and horizons. And the single most important thing you can do as a market participant is to know, honestly, which game you’re playing.

Part Five: Is Bitcoin an Investment or a Speculation?

With that framework in hand, let’s talk about Bitcoin. My purpose isn’t to attack Bitcoin or the people who own it. It’s to explain the puzzle from Howell’s chart: liquidity kept growing, yet the price fell. That points to the second half of the demand equation — the desire to buy Bitcoin — having changed. Why might it?

First, let’s be precise about what Bitcoin actually is. A Bitcoin is a unique entry in a decentralized digital ledger — essentially a number that can be verified and transferred from one holder to the next without a third party or permission from any central authority. The underlying distributed ledger technology, the blockchain, is a genuine innovation with real uses in financial services. Banks are using it; settlement systems are adopting it. The blockchain is real.

But Bitcoin itself — the thing you buy when you buy Bitcoin — raises a different question. What does it do? What income does it generate? What problem does it solve that isn’t already solved more efficiently by existing systems? What, exactly, does its value consist of?

In 2009, Bitcoin was pitched as a free-market alternative to government money — a currency governments couldn’t control, usable for peer-to-peer payments without banks or intermediaries. That was the vision. Seventeen years later, Bitcoin is still rarely used for everyday transactions. It’s too volatile — imagine pricing your groceries in something that can lose 30% of its value in a month. It’s slow, with transactions averaging around ten minutes to settle; fine for some purposes, useless for buying a cup of coffee. The vast majority of merchants don’t accept it, and most of those who do convert it to dollars immediately. It’s effectively banned in China. And governments the world over have repeatedly shown that they can and will tax, regulate, and restrict it.

These aren’t minor inconveniences. They go to the heart of what Bitcoin was supposed to be. As Professor David Rosenthal documented in a detailed late-2025 analysis, Bitcoin has failed to deliver on very nearly every promise made for it. (I went into this at length in my October 2025 video essay, “A Gaslit Asset Class.”)

So if Bitcoin doesn’t function as money and generates no income, what are you actually buying when you buy it? You are buying the expectation that someone else will pay you more for it later. That is a pure speculation. And now that the original use case has fallen short, the desire to own it appears to be withering.

Let me take you back to the 1990s, to a mania some readers lived through — and maybe took part in — while younger ones may never have heard of it: the Beanie Baby craze.

Beanie Babies were small stuffed animals from Ty Inc., retailing for about $5. Starting around 1996 and peaking in 1998–99, they became one of the great speculative episodes in American history. Individual ones fetched hundreds or thousands of dollars on eBay. People bought them by the case and stored them in plastic protectors, tags pristine — because a bent tag meant a “collectible” worth less. McDonald’s Happy Meal versions set off near-riots. Ty Inc. was pulling in $1.4 billion a year, and Ty Warner was worth an estimated $4 to $6 billion. A collector magazine selling 650,000 copies a month ran headlines like “How to Protect an Investment That Increases By 8,400%,” and some people put their children’s college funds into stuffed animals.

Then, in late 1999, Warner retired the entire line. The spell broke overnight. The secondary market collapsed, and buyers who’d paid thousands were left holding bags — literally, bags — of toys worth a few dollars each.

Before you laugh at the Beanie Baby buyers of 1999, though, set them beside Bitcoin buyers. Both assets generate essentially no income. Both attracted buyers chiefly because those buyers believed the price would keep rising. Both were wrapped in elaborate narratives about why they were uniquely valuable. Both pulled in a flood of new money — though from different places. Beanie Babies were funded mostly by small savers diverting money from other purchases and other collectibles like baseball cards and comics. Bitcoin, a far larger-scale asset, drew in institutional money, borrowed money, and money diverted from other investments. And both, at their peaks, convinced people they’d found an investment. They hadn’t. They were speculators who, for a while, were winning — until they weren’t.

Which brings me to Michael Saylor, and his company, which he pointedly named “Strategy.”

Strategy — formerly MicroStrategy — may be the purest expression of Bitcoin speculation in the public markets today. Here is what the company does: it borrows money by issuing convertible bonds and preferred stock (the preferred paying an 11% dividend) and uses the proceeds to buy Bitcoin. It has no operating revenue. It earns nothing from any business activity. Every dollar that comes in depends on selling common shares, preferred stock, and convertible bonds — which in turn depends entirely on Bitcoin’s price rising: rising enough to justify borrowing more to service the debt and the preferred dividend, rising enough to justify issuing more shares, rising enough to keep the whole structure from unwinding.

Strategy’s stock has historically traded at a premium to the value of its net Bitcoin holdings — the market valuing the shares above the coins behind them. That premium let Saylor issue new stock at inflated prices, use the cash to buy more Bitcoin, prop up the premium, and issue still more stock. As long as Bitcoin kept rising, the cycle turned.

Some analysts call this a “reflexive financial structure.” Others call it a Ponzi scheme. Pick whichever language you like. What I can say with confidence is that neither Strategy nor Bitcoin qualifies as an investment by any definition Benjamin Graham would recognize.

What kind of psychology sustains a belief that a structure like this can go on? Whatever the psychology was, it now seems to be changing. Bitcoin peaked in October 2025 and has since fallen about 50%. Michael Saylor, who only months earlier had famously vowed never to sell a single Bitcoin, recently sold roughly 3,600 of them at a loss — perhaps just to pay the bills. His net worth, which Forbes put at $7.4 billion near Bitcoin’s peak, had fallen to about $3.2 billion by June 2026.

Bitcoin is a novel object, but its pricing is not novel at all. You’ve heard of the 17th-century Dutch tulip mania, which peaked in 1637, when a single bulb might trade for the price of a horse and cart plus a small house. But at least the tulip bulb could grow a beautiful flower. At least a Beanie Baby could be handed to a child to play with. Both had some real use.

Can anyone explain to me, concretely, the use value of Bitcoin? Not the use value of blockchain technology — I’m asking about the specific asset called Bitcoin. What does it do? What problem does it solve? I’ve been asking that question for years, and I’ve yet to hear a satisfying answer.

Part Six: What’s Driving Today’s Stock Market

There’s a fog of half-understanding among economists about what pushes stock prices up. One camp holds that the quantity of money available to spend is the sole, or at least the primary, cause. This is essentially the naïve quantity theory of money — the idea that prices should rise in proportion to the money supply. People in this camp get confused when, say, the Fed creates trillions in new money and consumer prices barely move, as happened through the first decade of QE. What they miss is that, because of the motives and preferences of whoever received that new money first, it never really reached consumers at all. It stayed in the financial assets those first recipients wanted to buy.

That view ignores the second half of the demand equation — the human element, which decides where new money actually goes. Seeing rising asset prices alongside flat consumer prices, this camp concluded that maybe the quantity of money didn’t matter much after all; maybe it was something else, like falling interest rates. But falling rates don’t automatically lift asset prices. Only additional spending on an asset can lift its price.

The opposing camp says it’s all psychology — Keynes’s unpredictable “animal spirits” — that inflates the bubble. That’s inadequate too, because, just as at the cigar store, no asset price can rise unless buyers have more money to spend.

To restate the whole thesis: rising prices require rising demand, and rising demand requires both the ability to spend (more money available) and the willingness to spend it on the asset in question.

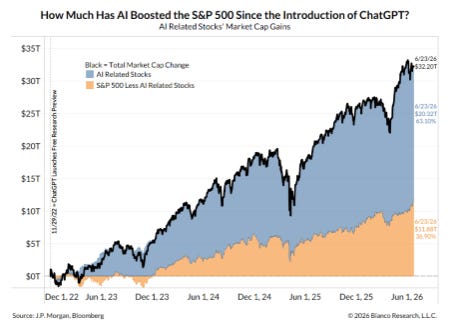

I want to close by applying this principle to today’s market, which is transfixed by artificial intelligence. Since November 2022, when ChatGPT first appeared, the S&P 500 has nearly doubled — up 96%. And 63% of that return came from the top AI names: about ten companies that now make up over 40% of the index’s market cap. Clearly, investors have more money to put into stocks — and they want to put an outsized share of it into AI.

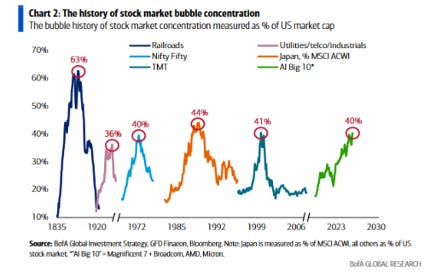

But is that investing, or speculating? The chart above, from Bank of America, tracks market peaks and the concentration of dominant investment themes over 150 years. Reading left to right: the railroad companies of the late 19th century, whose shares at their peak made up a staggering 63% of U.S. market capitalization; the telephone companies of the early 20th century; the “Nifty Fifty” of the early 1970s; the Japanese stock bubble of the 1980s; and the technology, media, and telecom (TMT) stocks of the late 1990s. Every one of those manias eventually imploded, and it took years — sometimes decades — for investors to recover.

The green line on the right is today’s top ten AI stocks. History suggests we have a major speculation underway. Caveat emptor.

I hope it goes without saying that I’m not knocking artificial intelligence. Far from it — AI is becoming a major driver of productivity. It helped me research this very essay. Its future is extraordinarily bright, and it may change the world the way the railroads or the fiber-optic buildout did. The question is not whether AI is real. The question is whether the price you pay for these AI stocks will be justified by their future earnings. I submit that today’s elevated prices reflect extreme speculation. Just as with the railroads and fiber optics, AI will deliver enormous benefits to its end users — while investors who bought in at these prices are likely to be disappointed.

But here’s the liberating part: you don’t have to buy these stocks, or the index, in order to invest in stocks. Instead of buying the market through an index fund, you can choose from a market of stocks.

That distinction is everything. The “stock market” — the S&P 500, the Nasdaq, the Wilshire 5000, any broad index — is a bundle. Buy an index fund, and you buy the whole thing, including the pieces trading at absurd valuations. But a “market of stocks” is something else: a universe of thousands of individual companies, many of which, even now, can be bought at reasonable prices relative to their earnings and dividends. Selective investing for real value is still possible. It takes more work than buying an index fund. It takes discipline and patience. But it’s available to anyone willing to do the homework.

After more than forty years of investing, I’ve reached a few conclusions I’ll share — not as prescriptions, but as the product of a long education in what works for me and what doesn’t. (This is a framework for thinking, not investment advice.)

First, I know I can’t predict which speculative asset will be the next big winner. I don’t think most people can either, though a few have done it, and others have been lucky enough to look like they did. Either way, good for them.

What I have been able to do is identify companies with durable businesses, growing earnings, and — my own preference — rising dividends, bought at reasonable prices. Dividend-growth investing has worked for me over a long career because it anchors my thinking in real economic value. With a solid dividend grower, I own a piece of a business that earns money and shares it with me. The price can swing all it likes, but the underlying reality of earnings and dividends provides a floor that pure speculation never offers. (Chapter Eight of A Black Hole in Economics goes deeper on this.)

You don’t have to invest exactly as I do. Some investors prefer companies that plow all their earnings back into growth rather than pay dividends — and for the right company, that’s a perfectly legitimate strategy. The principle isn’t dividends as such. The principle is this: buy assets whose value you can justify by reference to the income they generate, or the cash they’ll eventually return to you. That is investing. Everything else is speculation.

Which leaves a final question: are you an investor, or a speculator?

I’d urge you to be an investor. But whatever your answer — be honest about it.

“Like” this piece or perish in a cauldron of speculation.

HardmoneyJim, July 17, 2026

Jim, great post. I think for many of us, like myself, we fall into some middle bucket of investing and speculation. I think carefully about portfolio allocations and have owned no tulips, beanie babies or bitcoin, but...

For stocks, I rely on the advice of others because I feel I don't have the background to do what you do: individually pick. As you know, over the years, I've amassed S&P primarily because it avoids me having to pick. I think most people who have assets fall into this bucket.

I hope some day for a deep dive on how you pick, e.g., "I start by identifying an industry, then I identify the top 20 players in that industry by using X tool, then I look at ABCDE of those 20 companies using Y tool, then based on that analysis I narrow it 123 companies and pick 1 to buy if Z is true."

I made up that process, but perhaps it gives you the idea as to why when I read the following sentence in your post it feels like I'm staring into the black hole on your book cover:

"What I have been able to do is identify companies with durable businesses, growing earnings, and — my own preference — rising dividends, bought at reasonable prices."

For most people, I think, they have as much insight into sorcery as they do toward achieving what you describe. Maybe that's as it should be. Maybe only those who have practiced picking as a career, like you and Fred Hickey, should be picking. But... if that's wrong, and if there is a process that reasonably smart people can replicate with practice, a post on that topic would be powerful.

Great piece, Jim. One question, though, where does gold and gold mining stocks fit in this dichotomy?