Dollars To Donuts

Investing in bank stocks is riskier than Wall Street lets on

Here at HardmoneyJim, we’re all about money creation and what happens as a result. This naturally leads us to the money creators, the commercial banks. Intuitively, you might think the shares of the money creators could be comfortable investments. After all, they print money!

Your intuition would be wrong.

Take New York City Bancorp (NYCB), for example. “Regional lenders” like NYCB play a significant role in the US economy by providing around 40% of the financial for commercial real estate, with NYCB focusing on deals in New York City.

Here’s a two-year chart showing NYCB’s peak price per share of $13.66 eight months ago (July 2023).

Around the same time, JP Morgan decided to bump up NYCB shares to the top spot in the banking sector.

Funny enough, this upgrade happened right when NYCB hit its peak stock price of $13.66 in July 2023. But, as the rollercoaster price chart reveals, things quickly spiraled downward after that, with the stock taking a bumpy, unpredictable ride.

Despite the rough patch, some optimistic folks on Wall Street kept their hopes up. Even as NYCB dropped below $6 per share, a Piper Sandler analyst called NYCB stock "Very Attractive" on February 9. Fast forward to yesterday, March 4: Barrons reported on NYCB, stating, "NYCB Falls Hard After Credit Downgrades," even as most regional bank shares staged a dead-cat bounce. The stock closed today (March 5) at $3.22 per share, marking a 76% decline from its peak in July 2023.

It's hard to say if NYCB is going bust, but one thing's for sure: the Wall Street experts missed the mark on this one. Still, analyzing stocks is no walk in the park; not every investment pans out. So, shouldn’t we cut the JPM analysts some slack and write this flub off as a swing and a miss?

Yes, but there’s plenty more to consider when investing in bank stocks. Relying solely on a commercial bank's financial reports for your investment decisions is akin to gambling on a “black box” – a system that churns out results, but you have no clue how it actually operates.

Let me tell a story from yesteryear.

During the Great Financial Crash of 2008-9, I was a wide-eyed bank analyst at a Southern California asset manager. As the financial crisis unfolded, bank stocks nosedived. Our firm had invested some of our clients’ money in cheap bank stocks with names like Indymac, Countrywide, Washington Mutual, and Citigroup.

You might recognize Citigroup, but the others? They are history now and no longer exist. During 2008-9, my team and I watched, shell-shocked, as their share prices ratcheted lower. Gallows humor prevailed. To lighten the mood, we dubbed them “the donuts” – a nod to the shape of the numeral designating their final share prices. (Donut = Zero.)

While Citigroup survived with help from taxpayers due to its “too big to fail” status, the hit to its shareholders was as good as eating another donut.

Why didn’t we see it coming? We were relying on the financial statements of commercial banks, which are, to say the least, opaque. These reports are complex, ambiguous, and convey little real-time insight.

This is not the fault of the banks. Back in 2010, the CEO of a top-10 US bank told me over lunch that despite his 20 years in the banking business, he could not understand his firm’s financial statements thanks to the tangled accounting rules imposed by regulators. This fine gentleman understood his bank, but only because of his extensive inside knowledge of the operation.

So don’t blame the JP Morgan analysts for getting NYCB’s share price wrong. These are very smart people, among the best in the business. But when analyzing banks under financial pressure, “best in the business” is still not good enough. If you rely on public disclosure to value a bank that’s under stress, you might as well try to hit a fastball wearing beer goggles.

If the bank’s published numbers didn’t tell you enough, how could you have known NYCB was a bad bet? You might never have known for sure, but some available clues did not appear in the bank’s financial statements.

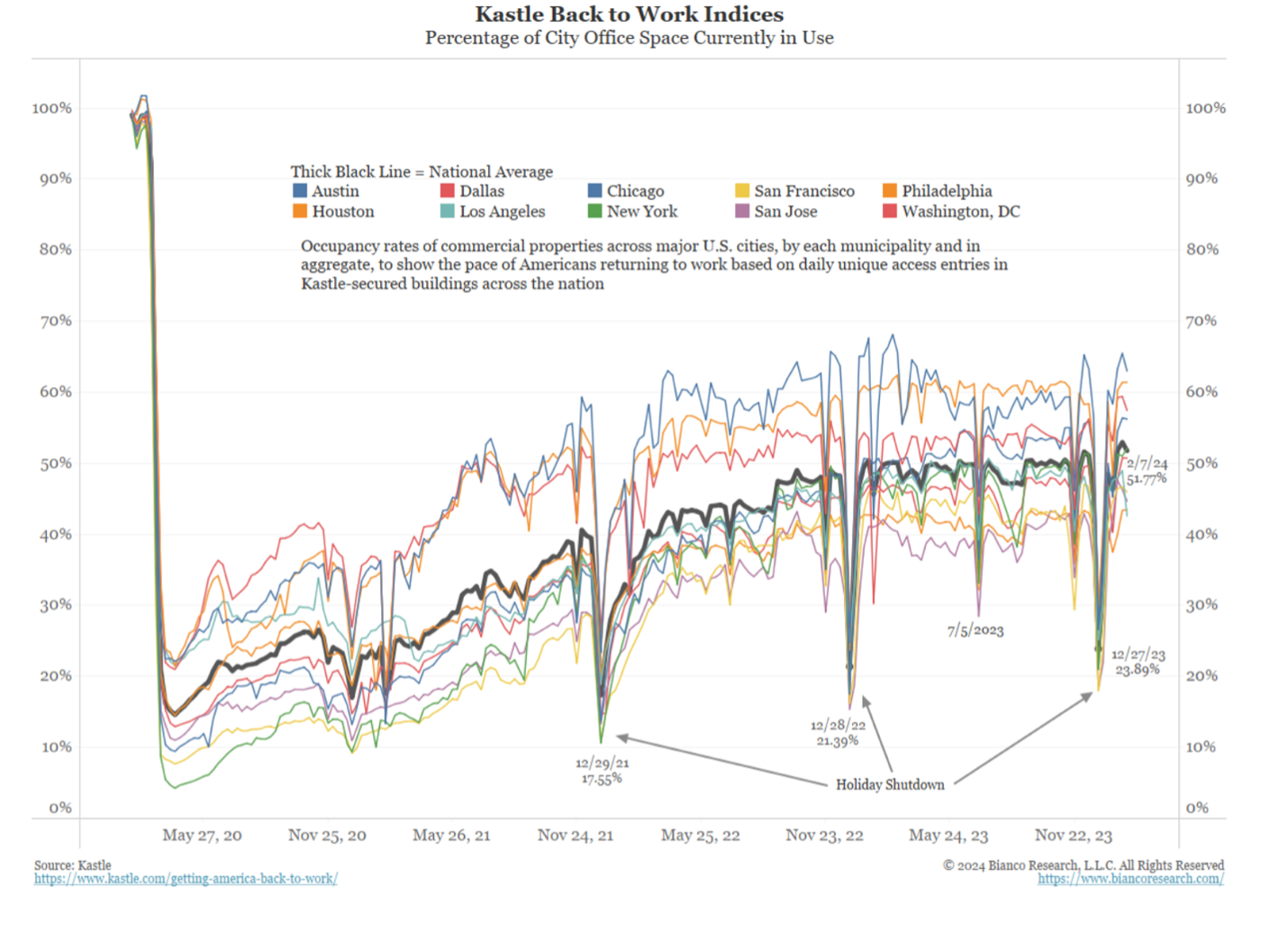

Here’s one example: Kastle Corporation, a nationwide distributor of card-key swiping systems, has a unique vantage point to assess commercial real estate occupancy trends. Their graphical analysis, easily accessible to Wall Street, paints a grim picture of major city commercial properties.

According to the data in the graph, following the onset of the COVID-19 pandemic, the average occupancy rates in downtown real estate sharply declined. Despite some recovery, the rates have plateaued at just 50% of their pre-Covid levels.

(The graph is from Bianco Research; subscription required.)

Four years of half-empty cities is a long trend, but the financial consequences of “work-from-home” are just now showing up in NYCB’s loan losses. A modest proposal: Patiently watching data like this would have kept a conservative investor out of the regional banks.

Let's face it: the COVID lockdowns really shook things up, changing what we once took for granted. The economy is in a different place now—not all bad, just different. One significant change from pre-COVID to now is how quickly the work-from-home trend, which was already in place, picked up steam during the lockdowns. Judging from Kastle's data, it doesn't appear we are going back to the office anytime soon. Those hoping for things to snap back to pre-COVID "normal" might be in for a rude awakening.

NYCB is undoubtedly highly exposed to this whole empty office situation. It's tough to picture the JP Morgan analysts sticking their necks out for the stock if they had gotten a peek at the Kastle data - unless, like me back in 2008, they put too much trust in the banks’ public financial reports. The warning signs about the commercial real estate mess were there in the Kastle data many months ago, while the banks are just starting to reflect the stress in their financial statements.

Here’s another example of available evidence you can use to avoid disaster. It’s anecdotal, but it’s significant. From a Zerohedge report:

According to the report, Canada’s largest pension fund walked away from a multi-million dollar building and handed the keys back to the bank. It’s reported as a one-off incident, but it likely signals a systemic problem because if you have seen one cockroach, you have not seen them all. This cockroach is telling us the office building glut is not over, and it may be a while before it’s safe for ordinary people to invest in the companies that own or lend to these buildings.

The point is that data available just by looking around may be more informative than trying to penetrate the black box of bank financial statements. The guys at JP Morgan are very smart, and so were those at my firm in 2008. But we got it wrong because of our myopic concentration on financial statements. We’d have been better off listening to barbershop chatter about which banks suffered the most withdrawals. At least that would have been real-time data.

Is there widespread fraud lurking in the balance sheets of these troubled regional banks? Possibly, but I doubt it. The stress in NYCB’s loan book is more likely due to years of easy money, inflated asset prices, and a work-from-home trend accelerated by government lockdowns. Everything has changed for the investors who bet on these projects. Any “fraud” likely came from the Fed and Fauci.

Will depositors at New York City Bank lose money? Definitely not. Even though about 45% of bank deposits are not FDIC insured, the Fed is committed to making all depositors whole, as they did after the March 2023 failure of Silicon Valley Bank, Signature Bank, and First Republic Bank. Not a single depositor lost a penny or even suffered a delayed payout. I am not saying this policy is healthy for the banking industry or the economy, but it is a fact and it is what the Fed will do.

Does the real estate problem at NYCB signal a looming banking crisis? There is undoubtedly a “crisis” for the shareholders of banks with significant exposure to commercial real estate. And there soon may be more examples of “dollars turning into donuts” among regional bank shares, like this one:

Dollars To Donuts – Silicon Valley Bank Share Price:

But that does not mean the entire banking system is poised for a meltdown. The regional banks’ problems are significant, but the regulators and the money-printers-of-last-resort at the Fed will contain them. Expect more bank mergers, as the Treasury and the Fed encourage the strong banks to devour the weak. And the Fed will be right there with “selective QE,” monetizing the under-water assets of troubled banks. (See my March 31, 2023 article, “Why Is The Failure Of Silicon Valley Bank Important?”)

The bottom-line lesson for investors is: sometimes what you don’t own keeps your fortune whole. As I said here, I would avoid investing in long-term government bonds, given that Uncle Sam will have to pay its debt in depreciated dollars. I will now add that I’d also avoid investing in the black box of commercial banks unless you somehow feel very confident that you know what's in that box.

Thanks for reading HardmoneyJim!

March 5, 2024

Spare your friends the agony of turning dollars into donuts! “Like” this piece and pass it on!

Interesting post (as usual!)! I recall from previous posts/videos the recommendation of: real estate, gold, mining stocks, energy stocks. Perhaps I'm missing something from your original list.

Here you warn against banking stocks and long-term treasuries. By omission, does that mean you think short term treasuries are a good place to park money now? Thank you!